OECD Economic Outlook – March 2025

- Economy, Global, Research

Steering through uncertainty

Introduction

The global economy remained resilient in 2024, expanding at a solid annualised pace of 3.2% through the second half of the year. However, recent activity indicators point to a softening of global growth prospects. Business and consumer sentiment have weakened in some countries. Inflationary pressures continue to linger in many economies. At the same time, policy uncertainty has been high and significant risks remain. Further fragmentation of the global economy is a key concern. Higher-than-expected inflation would prompt more restrictive monetary policy and could give rise to disruptive repricing in financial markets. On the upside, agreements that lower tariffs from current levels could result in stronger growth.

Key figures

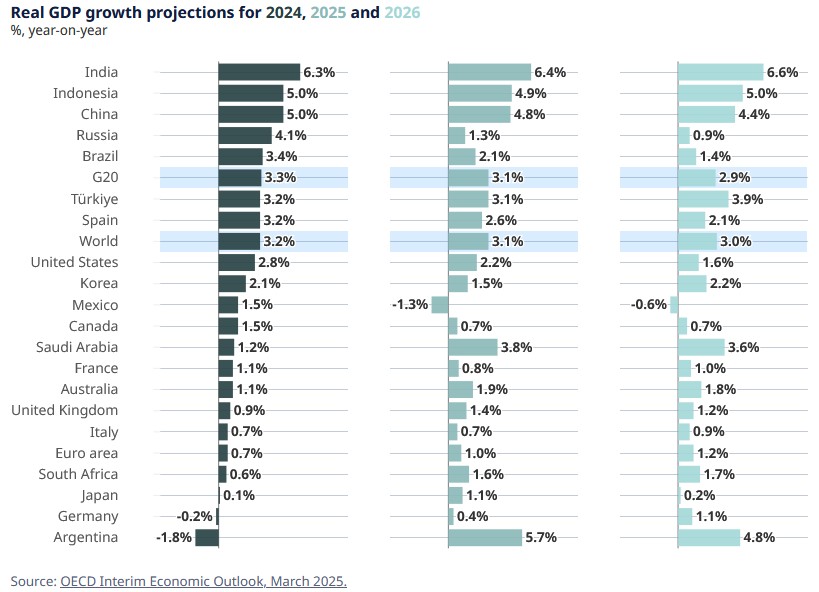

Global growth is projected to moderate

Global GDP growth is expected to moderate from 3.2% in 2024 to 3.1% in 2025 and 3.0% in 2026, with higher trade barriers in several G20 economies and increased policy uncertainty weighing on investment and household spending. Annual real GDP growth in the United States is projected to slow from its very strong recent pace, to 2.2% in 2025 and 1.6% in 2026. Euro area real GDP growth is projected to be 1.0% in 2025 and 1.2% in 2026, as heightened uncertainty keeps growth subdued. Growth in China is projected to slow from 4.8% this year to 4.4% in 2026.

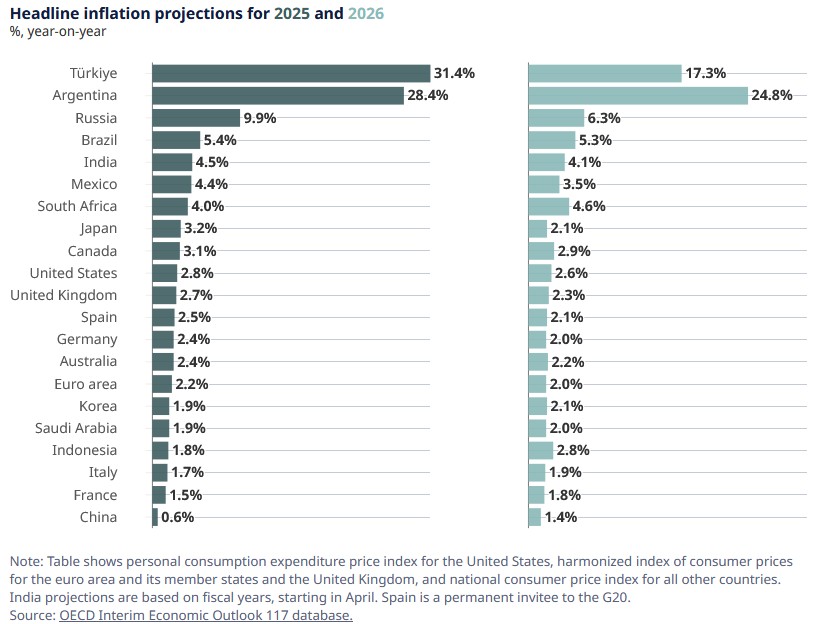

Inflation continues to linger in many countries

Inflationary pressures persist in many economies, with headline inflation recently turning up again in an increasing share of economies. Services price inflation has stayed elevated, with a median rate of 3.6% across OECD economies. Over 2025-26 inflation is projected to be higher than previously expected, although still moderating as economic growth softens. Headline inflation is projected to fall from 3.8% in 2025 to 3.2% in 2026 in the G20 economies. Underlying inflation is now projected to remain above central bank targets in many countries in 2026.

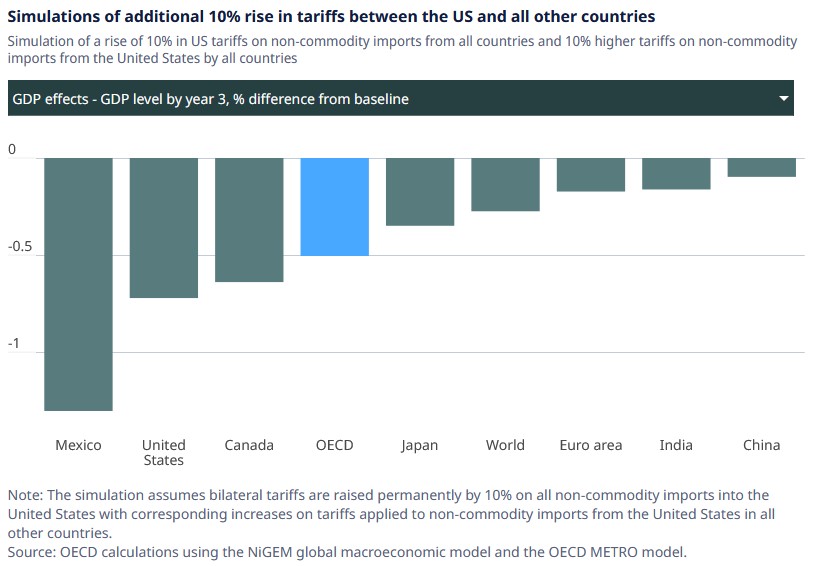

Further trade fragmentation would harm global growth prospects

The high level of geopolitical and policy uncertainty at present brings with it substantial risks to the baseline projections. One possible risk is the escalation of trade restrictive measures. An illustrative exercise, where bilateral tariffs are raised further on all non-commodity imports into the United States with corresponding increases in tariffs applied to non-commodity imports from the United States in all other countries, shows that global output could fall by around 0.3% by the third year, and global inflation could rise by 0.4 percentage points per annum on average over the first three years. The impact of these shocks would be magnified if policy uncertainty were to increase further or there was widespread risk repricing in financial markets. These would add to the downward pressures on corporate and household spending around the world.